Central banks' appetite for the precious metal is growing

The actual level of public procurement may be much higher than the official level

On October 31, the World Gold Council (WGC) published data on the global gold market for the third quarter of 2023 on its website. The situation in the world market of precious metals is closely related to the global financial markets by direct and inverse dependence. WGC data is therefore important not only to narrow gold specialists, but also to anyone following general trends in the global economy and international finance.

The LBMA (London Bullion Market) average gold price in the third quarter was $1,928.5 per ounce. While it was 2% lower than the record high seen in the second quarter, it was still 12% higher than in the third quarter of last year. Several countries, as noted in the WGC report, saw price increases in local currencies due to currency weakness against the US dollar. The report mainly names countries such as Japan, China and Turkey. But I would also add Russia, where the ruble exchange rate broke the 100 ruble per dollar mark in mid-August. If on August 1 the price of gold (set by the Bank of Russia) was 5,754.8 rubles per troy ounce, then on August 15 it rose to 6,223.5 rubles (an increase of 8.2%). By the end of the third quarter, the ruble price of gold had not returned to its original positions. On September 30, it was equal to 5,867.9 rubles per troy ounce.

In terms of gold production, the third quarter of this year turned out to be a record for the period of monitoring the market since 2010 (971.1 tons were extracted from the bedrock). The world production of the precious metal in the first three quarters of the year also turned out to be a record (2,744 tons). The increase in production in the 3rd quarter of this year compared to the 6th quarter of last year was 14 percent. This was achieved by increasing production in the following four countries: Canada (by 14%), the USA (by 13%), Ghana (by 7%) and Australia (by 3%). At the same time, a reduction in production was recorded in the following countries: Mexico (by 15%), Tanzania (by 14%), Sudan (by 10%) and the Russian Federation (by 4%).

The WGC report states that the drop in production in Russia was mainly due to the largest field in our country "Olimpiada" developed by Polus. WGS notes that this appears to be the result of business decisions rather than Western sanctions imposed on the company. "These sanctions do not appear to have a significant impact on the volume of gold production" the document said.

At the end of last year, the leaders of world gold mining were the following three countries: China (374 tons); Russia (330 tons); Australia (320 tons). It is possible that Russia will move to third place by the end of this year.

The supply of the precious metal to the world market is ensured not only by the extraction of gold from the subsoil, but also by its secondary production - the processing of waste containing the precious metal. At the end of the third quarter, the volume of this secondary gold production was 288.8 tons, which is 8 percent more than in the third quarter of last year. The total supply of gold on the world market (mining + secondary production) increased by 6% year-on-year in the third quarter of 2023.

Gold demand in Q3 was as follows. The main buyer of the precious metal has traditionally been the jewelry industry (578.22 tons). It absorbed gold in a volume roughly equal to half of total demand. Investment in precious metal in the form of purchase of bullion and coins -295.19 tons. Purchase of gold for the production of electronics and other equipment -75.29 tons.

Exchange-traded funds (ETFs) have been a significant buyer of gold for many years. However, since last year, these funds have turned from net buyers to net sellers. In the third quarter of last year, net sales of the ETF amounted to 243.7 tons, according to the results of the third quarter of this year, net sales amounted to 139.3 tons. ETFs are funds that can be called speculative rather than investment funds. In the spring of last year, central banks began to move sharply from the policy of "quantitative easing" to the policy of "quantitative tightening". This was done under the pretext of fighting against uncontrollable inflation in the world and it was manifested by an increase in key rates. Interest rates on many securities and other financial instruments have started to rise. ETFs began to shake up their investment portfolios, replacing gold with highly profitable securities. Most of the substitutions have already been made by these funds, so net sales of gold ETFs in the third quarter of this year are 43% lower than in the third quarter of last year.

But there is another important component of the demand for the precious metal that I want to talk about in more detail. It is about demand from central banks. In the era of the gold dollar standard (which was established after World War II by the International Monetary and Financial Conference at Bretton Woods in 1944), central banks were the main buyers of the precious metal. Their foreign exchange reserves were created at the expense of two main components - the US dollar and monetary gold (standard bricks, partly gold coins). The peak of purchases of the precious metal by central banks was in the 1960s. True, one country's gold reserves were falling. It was the United States of America. Under the terms of the Bretton Woods agreement, they agreed to exchange dollars for precious metal to the monetary authorities of other countries. In the 1950s, US gold reserves sometimes exceeded 20,000 tons, but by the end of 1960 they had dropped to 9,000 tons.

At the initiative and under pressure from the United States, the gold-dollar standard was replaced by the paper-dollar standard. The decision was made in January 1976 at the International Monetary and Financial Conference in Jamaica. Under pressure from the United States, the monetary authorities of many Western countries began to sell the metal from their international reserves. From the late 1970s to the beginning of the last decade, central banks around the world acted as net sellers of gold. If readers wish, they can learn more about the history of gold in this period from my book "Gold in the World and Russian History 2017-2008 Century". (Moscow: Rodnaya strana, 2009). I write in it that the global financial crisis of 2008-2009 led to a reversal of the long-term trend, since 2010 the central banks of the world have changed from net sellers to net buyers of the precious metal. The global financial crisis showed the fragility of the policy of creating international reserves only at the expense of dollars, euros and other so-called "reserve" currencies.

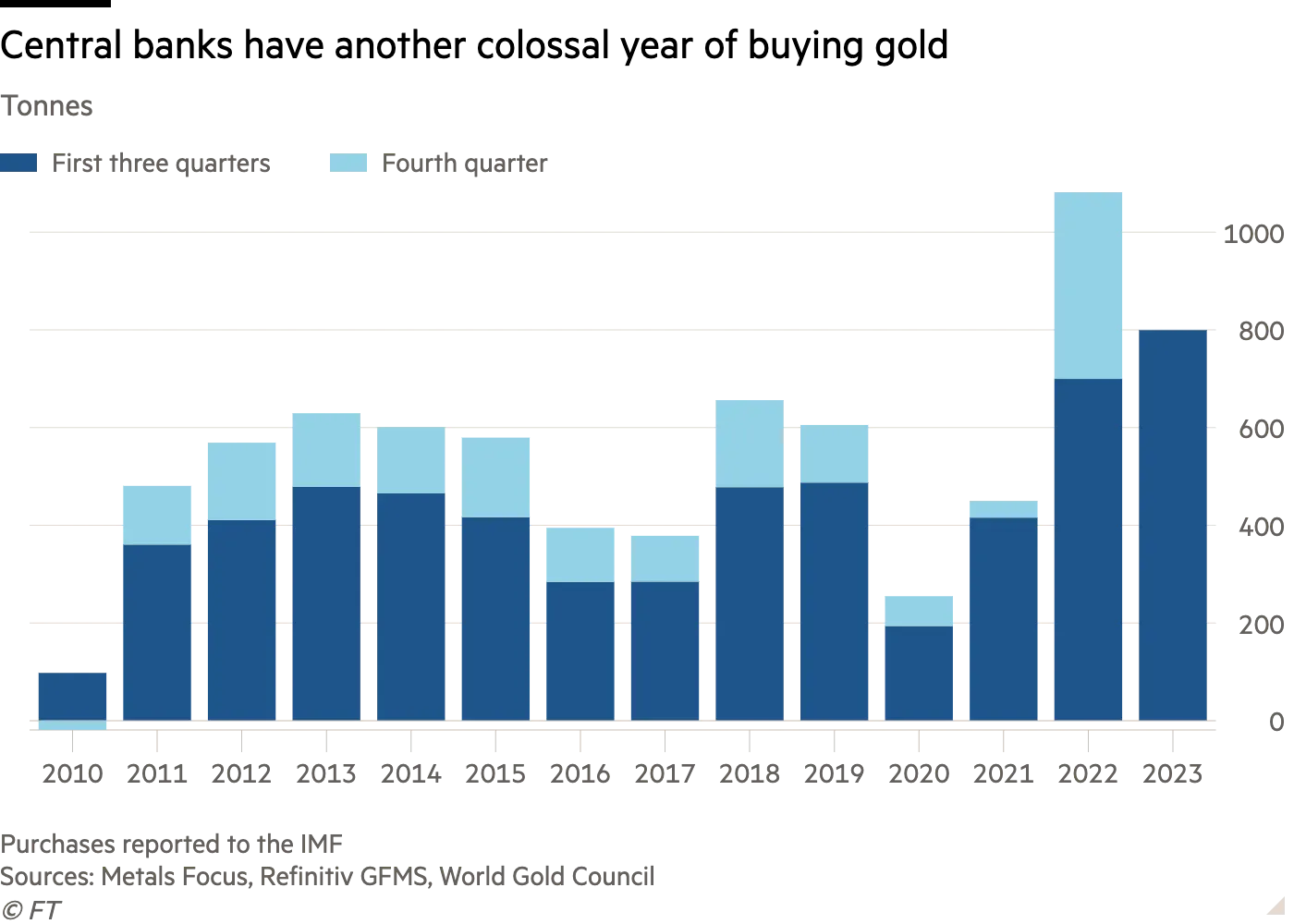

Let's go back to the WGC report. At the end of the 3rd quarter, net gold purchases by central banks were 337.1 tonnes (up 120% from the previous quarter). This is the second highest quarterly figure for all years of observation (the record was the 3rd quarter of last year - 458.8 tons).

And according to the results for the three quarters of this year, net purchases of the precious metal by central banks reached the level of 800 tons. That's a 14% increase over last year and a decades-long record since the late 1960s. So far, it is difficult to say whether a record will be reached at the end of 2023. However, the probability is high.

Let us recall that at the end of last year, central banks bought a record volume of the precious metal since the late 1960s – 1,081 tons. For a new record to be set, net purchases of the precious metal by central banks in the fourth quarter of this year must be more than <> tonnes. In any case, we see that central banks are rapidly increasing their gold reserves and the share of the precious metal in the total volume of foreign exchange reserves is growing.

The WGC's four central banks are among the most active gold buyers in the third quarter. The leader in buying the precious metal was the People's Bank of China (PBOC), which increased its gold reserves by 78 tons in the third quarter. Since the beginning of the year, the volume of gold reserves of the Central Bank of China has increased by 181 tons to 2,192 tons. In value terms, this corresponds to 4% of China's foreign exchange reserves.

Second place in terms of purchases was occupied by the Polish Central Bank, which bought 57 tons of gold in the third quarter. Poland thus stores 334 tons of gold, which is 11% of total reserves. Warsaw plans to increase this share to 20%.

Turkey completes the first three, whose central bank bought 39 tons of gold in July-September. Turkey has traditionally been a major buyer of the precious metal to replenish its international reserves. However, it has had to sell off gold from its international reserves in the last few quarters. Turkey is trying to compensate for the losses incurred. However, at the end of the third quarter, its gold reserves were still 12% lower than at the start of the year.

Other net buyers of gold in the third quarter were the central banks of the following countries: India (9 tonnes), Uzbekistan (7 tonnes), the Czech Republic and Singapore (6 tonnes each), Qatar and Russia (3 tonnes each), the Philippines (2 tonnes) and Kyrgyz Republic (1 ton). There were other central banks that acted as buyers, but their net purchases of the precious metal were less than one tonne.

The only significant seller of gold in the third quarter was Kazakhstan, which sold 4 tons of gold. The WGC report also mentions Bolivia "cashing out" 17 tonnes of its gold reserves between May and August.

Notably, the WGC has been clarifying in its statistics on purchases and sales of gold by central banks for several quarters now that the figures reflect "registered" transactions. As a result, secret operations of the central bank with the precious metal are also carried out, which are not reflected in national statistics. At the same time, the WGC acknowledges that its statistics may differ significantly from the actual picture. By the way, experts have been saying for many years that China can make large-scale purchases of gold to replenish international reserves, in transactions that are not registered (and therefore not reflected in official statistics). But after the launch of the Russian special military operation in Ukraine, Western media increasingly suggest that the same "unregistered transactions" could be carried out in the Russian Federation.

In the WGC thread, citing Bloomberg, there were reports in early August that Russia would resume purchases of foreign currency and gold, "but no further details on the volume and timing of future purchases have yet been received.".

Yesterday (31/10/23) the Financial Times, just after the WGC report, published an article entitled "China leads record central bank gold purchases in first nine months of year".

As the Financial Times notes, there is reason to believe that the actual level of purchases by central banks—especially Chinese and Russian—was much higher than officially reported: "Central banks report gold purchases to the IMF, but global flows of the yellow metal suggest that the actual level of purchases official financial institutions, especially China and Russia, was much higher than officially stated."

The article also notes that the Arab-Israeli conflict, which began on October 7, will be (already has become) a significant factor in the growth of the price of the precious metal. I would like to add that on October 6, the day before the conflict began, the price of gold hit a seven-month low of $1,809.50. per troy ounce. After the conflict started, it quickly broke the $2,000 mark. However, by the end of the month, prices stabilized somewhat ($1,986.3). However, according to experts, by the end of the year, the price may stabilize above the 2,000 thousand dollar mark per troy ounce.