Vulnerability of US banks to growing systemic risks

The Federal Reserve has been sending very mixed signals lately.

Last week on November 1, after the meeting of the Federal Open Market Committee (FOMC), Jeremy Powell reported that the banking system is strong and that the central bank of the United States FED has essentially no concerns about the liquidity of small and medium regional and even large banks and their ability continue with your business.

He more or less assured that the banking sector is as strong as it can be, especially after the collapse of SVB Bank earlier this year. But in its next post, the Fed subsequently convinces us that the US banking system is still vulnerable. But the good news is that it is less vulnerable than it was before the 2008 crisis. So we should be calm.. But the situation may not be as good as they tried to convince us last week.

But nothing new happened that week that could justify this change in Powell's statement and the Fed's statement, since both are probably based on the same source of information.

So what are the issues we should be aware of? The New York Federal Reserve System (FED) says there are growing vulnerabilities in the banking sector related to funding and capital shortages. The central bank says risks to the banking sector are slowly increasing. In the same post, the Federal Reserve also pointed out that based on data from the second quarter of this year, large banks do not appear to be at risk as much as small and medium-sized banks.

FED says above:

"The bank failures that occurred in March 2023 highlighted how unrealized losses on securities can make banks vulnerable to a sudden loss of funding."

Sudden loss of funds, these are extremely disturbing words in banking.

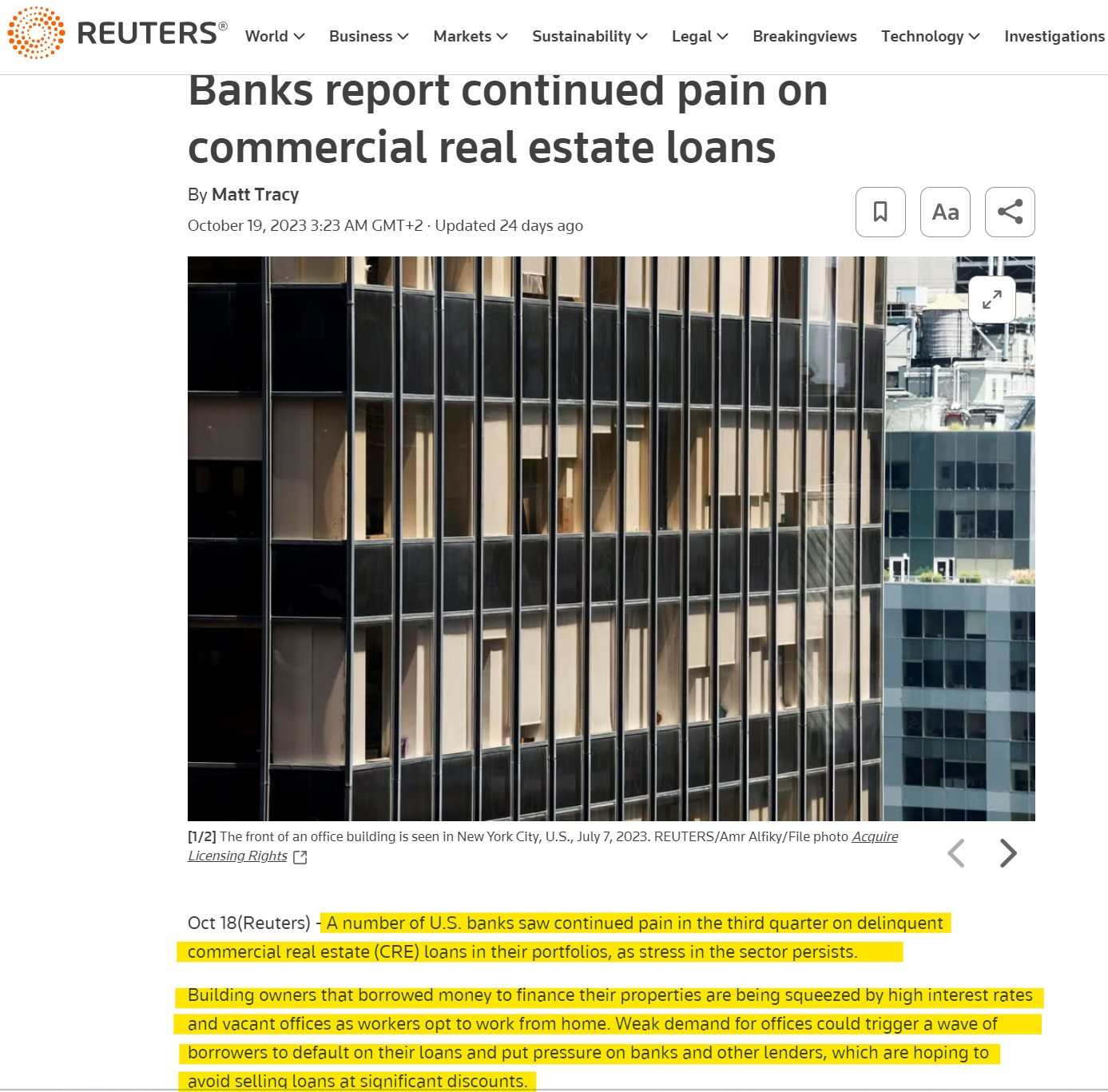

Reuters recently reported on the difficulties in the banking sector. As difficulties in the sector persist, a number of US banks continued to make payments on delinquent commercial real estate loans in their portfolios in the third quarter. Building owners who borrow money to finance their properties are being squeezed by high interest rates and office vacancies as businesses and workers continue to choose to work from home. Weak office demand could trigger a wave of borrowers defaulting on their loans, putting pressure on banks and other lenders hoping to avoid selling loans at deep discounts. Selling off the loan at a discount would cause significant losses to the banking sector of around 70%. All small and mid-sized US banks are thus at risk because of their significant investment or exposure to these loans in commercial real estate, which is declining in value due to extreme vacancy rates.

And this is a real iceberg, but it's still completely underwater and I still can't see its top. And why? As these loans are not due yet.. they will start maturing next year starting 2024..!

A game with numbers..

Results for the third quarter showed that the big banks posted higher earnings in the period, which was seen as great news and reassurance that the banking industry is indeed doing well. However, the increase in income is actually mainly driven by higher interest rates, not by an increase in demand for banking products such as loans. News headlines are truly deceiving.. In fact, banks were increasing their reserves to cover expected losses from bad loans and rising delinquencies..

A report from Reuters explains more details about the third quarter - Morgan Stanley booked $134 million in loan losses. Similar to the second quarter, when it set aside $161 million, the bank noted that this was due to "deteriorating conditions in the commercial real estate sector".

Other banks' profits showed similar problems. Goldman Sachs announced that this year alone it reduced its exposure to commercial real estate (CRE) by around 50%, and it could happen that if we looked more deeply, into the financial statements, this 50% the decline must result in a substantial loss..

Another major systemic bank, Bank of America, also reported the same day that its nonperforming loans, or loans at least 90 days past due, rose to nearly $5 billion in the third quarter from $4.27 billion in the second quarter, largely due to its portfolio Office Names (CRE)..

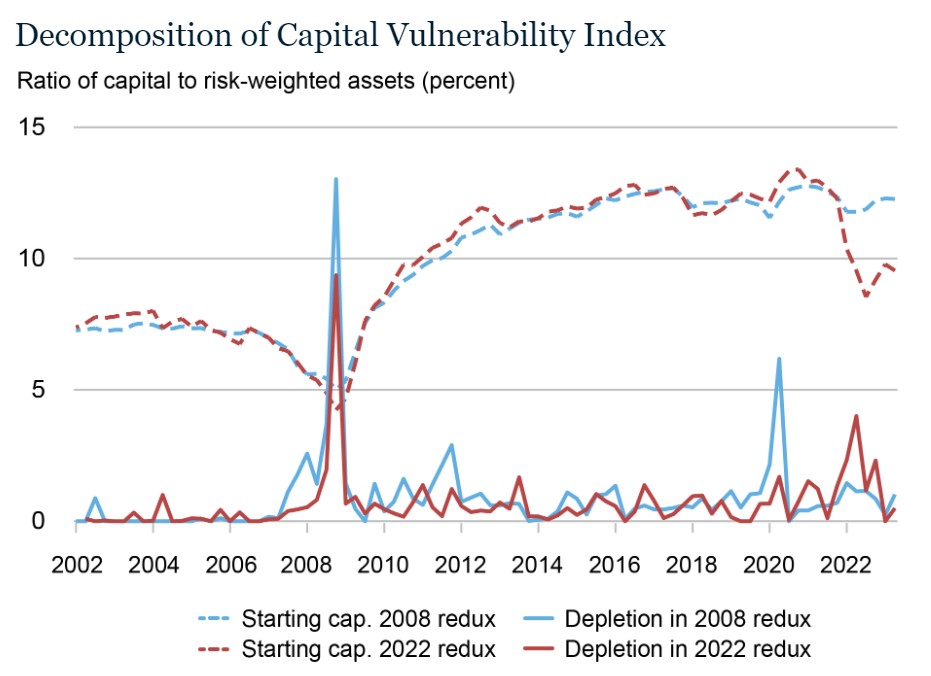

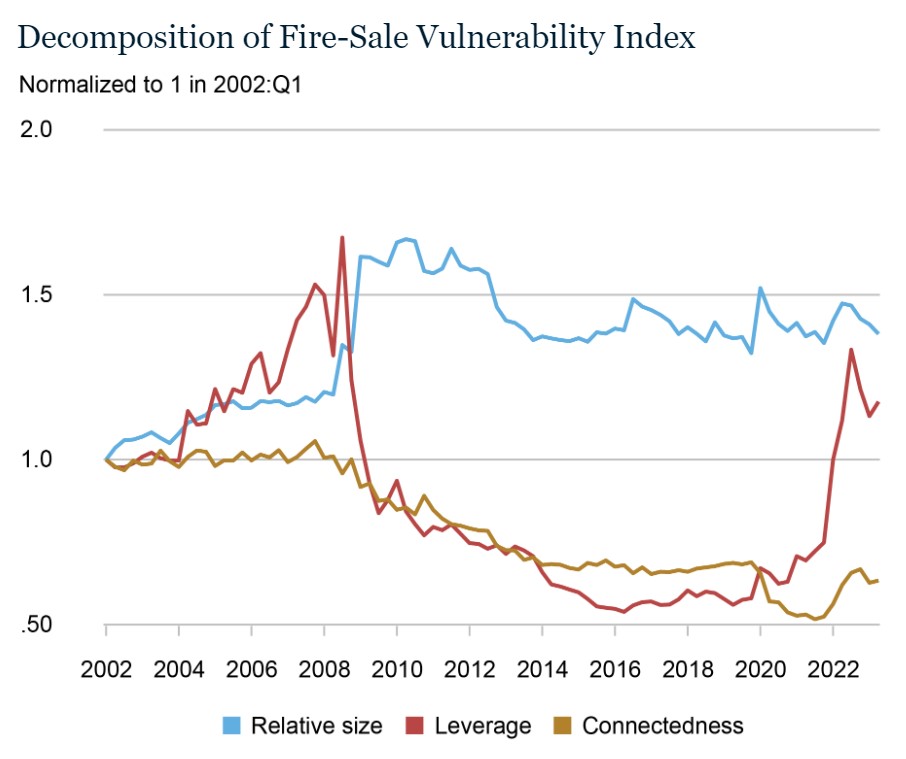

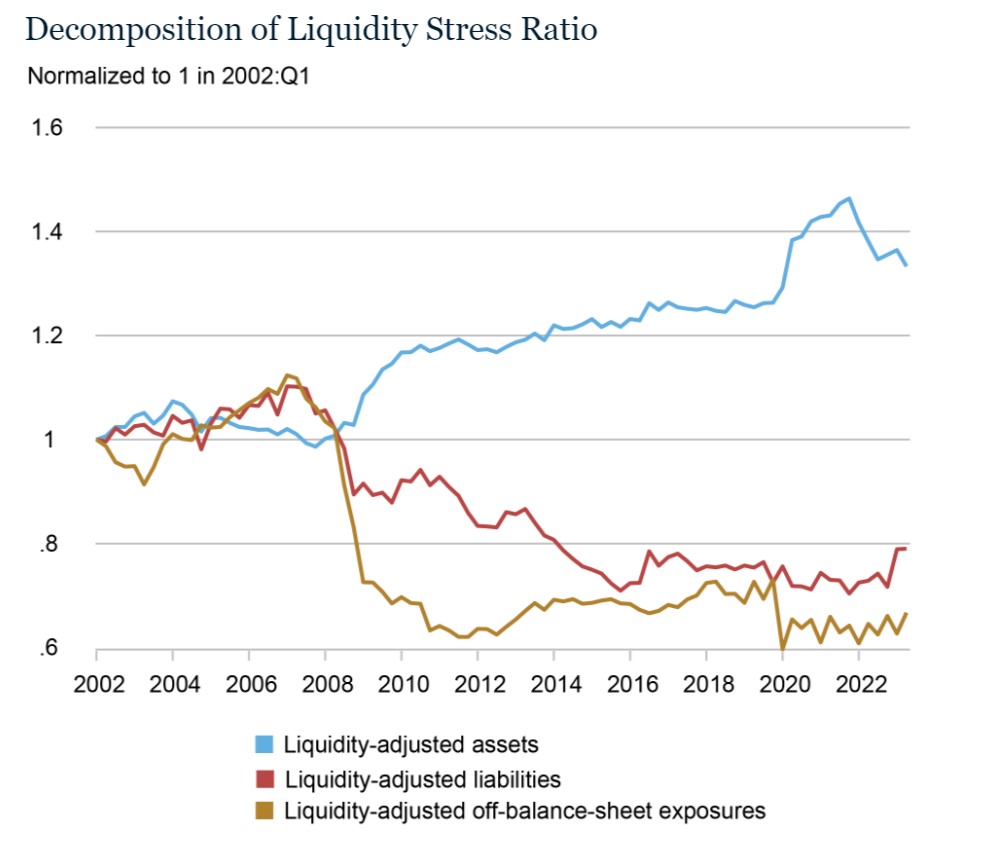

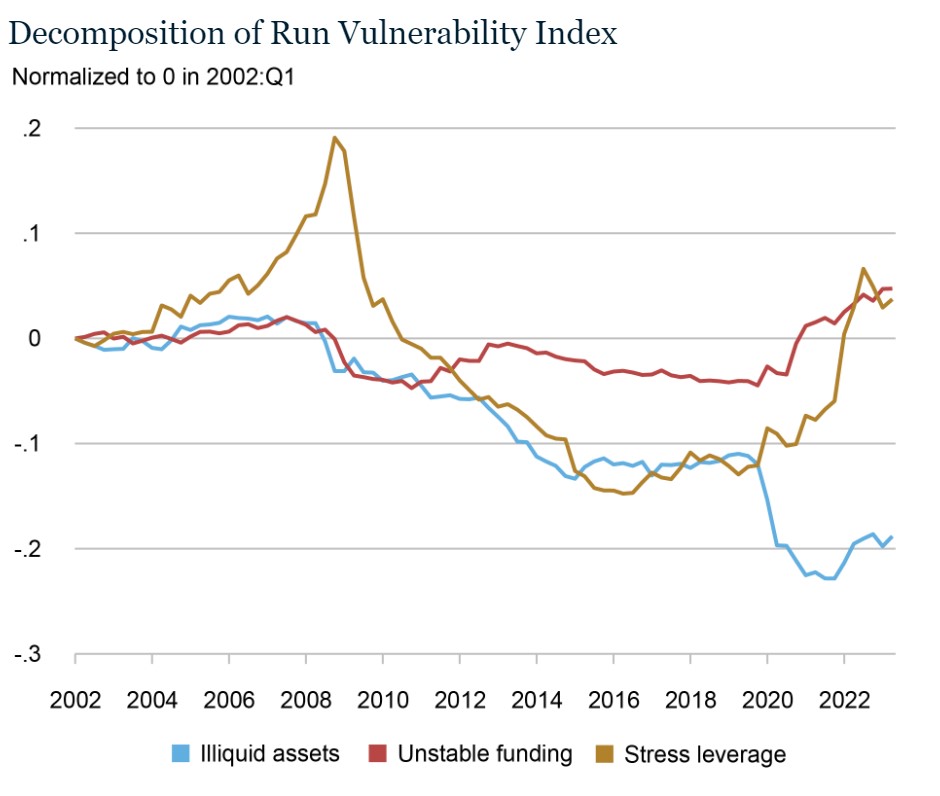

The Federal Reserve System (FED) also explains how to measure the vulnerability of the US banking sector in four steps:

- Capital Vulnerability Index

- Fire-Sales Vulnerability Index

- Liquidity Stress Ratio

- Run Vulnerability Index

We will not go into the details of what each index and ratio means, but it is clear from the graphs that starting at the end of 2022, all four values rise and show a sharp increase. This is bad news and we see it growing further in 2023 based on the information above.

In addition to concerns about liquidity, there are also large volumes of cash withdrawals from depositors. This proves that confidence in the banking system is low. When we combine this with the problems of commercial real estate, it is a very worrying signal. We can already see this in the slight increase in System Vulnerability Indices compared to their low level over the last 10 years.

Thus, in the short term, banks could suffer losses in their securities portfolios, which could subsequently cause funding to dry up and effectively weaken effective capital levels. If clients bank with a small or regional bank or credit union, it will be important for them to monitor their level of exposure to commercial real estate loans as well as what other clients are doing in case there is a large outflow of deposits.

Let's hope that this will not be the case, but it is definitely worth monitoring with caution, because the European banking system is linked to the American one, and so these effects will quickly be reflected on our continent as well.

The following year will give us a clear answer as to what impact the loans due in 2024 will have, if there will be bankruptcies of corporations and banks, as I wrote in the previous article.

But we can prepare for it. One of the options for this is the so-called asset diversification, using the Permanent Portfolio - dividing your assets into three to four parts:

- cash, stocks, bonds, retirement saving, ...

- real estate

- precious metals - gold, silver, platinum

- cryptocurrencies - bitcoin and ethereum

Michal