The collapse of two more banks, the risks of the effects of unrealized losses and rising unemployment...

Recently, there are more and more signals that the global financial system and the entire banking sector are on the verge of breaking events. An example of one of the signals is, for example, the fact that Jamie Dimon, the CEO of the largest bank in the world, JP Morgan Chase, plans to sell part of his shares (11.6%) in 2024 as part of the diversification of his portfolio. Jamie has been with this banking giant for many years and it is one million shares worth $141 million.

Despite this, the FED, ECB and other central banks keep the same "line" in every speech and assure us practically every week that the banking industry is strong and resilient.

Last week, however, another red signal was added - the Federal Deposit Insurance Corporation (FDIC) released a report stating that there are $684 billion in unrealized losses on the books of American banks.

This trend of increasing unrealized losses continues, and it is not just US banks, but the global banking sector.

Unrealized losses

As the name suggests, this is a loss from an asset that has not yet been sold or disposed of. In practice, an unrealized loss can be considered a paper loss, but once that asset is sold, the loss becomes realized and appears on the income statement. If banks purchase securities, they do not have to regularly record them in the statement at market value. In accounting, they are kept only at their purchase price, and thus an unrealized loss arises, which is the difference between what the market is now willing to pay for these securities and what the bank paid when it bought them.

US banks are currently sitting on $684 billion worth of unrealized losses. If they were to be implemented all at once, the banking system there would collapse.

According to the latest quarterly report of the Federal Deposit Insurance Corporation (FDIC), it follows that unrealized losses on US government bonds and held-to-maturity securities at US banks increased by 22% in the third quarter, i.e. by $126 billion, and the total amount of unrealized losses so as of September 30, it reached the aforementioned 683.9 billion USD.

Now imagine what that number would have been if the FDIC had not taken over the bankrupt SVB, Signature Bank and First Republic Bank in March of this year. The three banks had significant unrealized losses on their books.

And just by the way, while we're talking about failed banks, did you know that two other American banks went bankrupt?

- Heartland Tri-State Bank went bankrupt on July 28

- and Citizens bank on November 3

The Fed's aggressive interest rate hikes are probably the main reason why US banks are sitting on hundreds of billions of dollars worth of unrealized losses. Banks invested in bonds when interest rates were low. After that, however, the FED increased rates, which resulted in a decline in the value of both types of securities, held-to-maturity and marketable securities. Since the total balance of $684 billion is technically unrealized. Banks can keep them on their books until the securities mature, in which case this problem would of course disappear entirely.

However, this is a very unlikely scenario. This is because there are many banks that cannot afford to hold these securities for much longer, especially if there are any other negative market events where they will need access to cover them and further funding. In order for banks to function, they must be liquid... And in order for the bank to obtain this liquidity, it would be forced to sell these depreciated securities at a loss, where the unrealized losses would be realized in the amount of millions to billions of dollars.

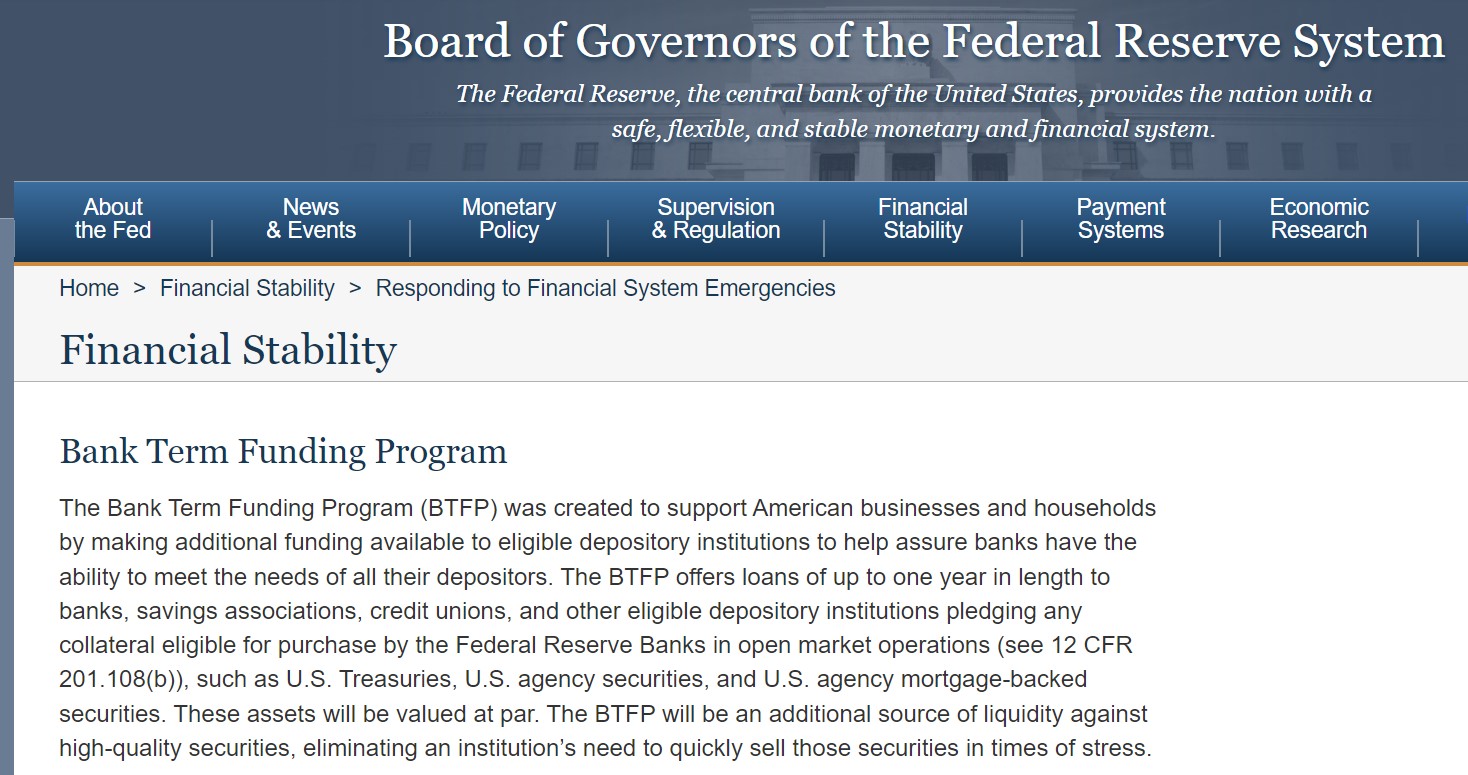

Bank Term Funding Program (BTFP)

So far, the banks have managed to deal with the unrealized loss thanks to the fact that they could borrow from the Fed's program called "Bank Term Funding Program". This is a short-term bailout program from which the Fed allows banks to borrow money using their securities that have lost value and would now incur significant losses if sold.

This program is really just a band-aid, it doesn't really solve any deeper problems, it just buys more time and thus the continuation of the growth of unrealized losses.

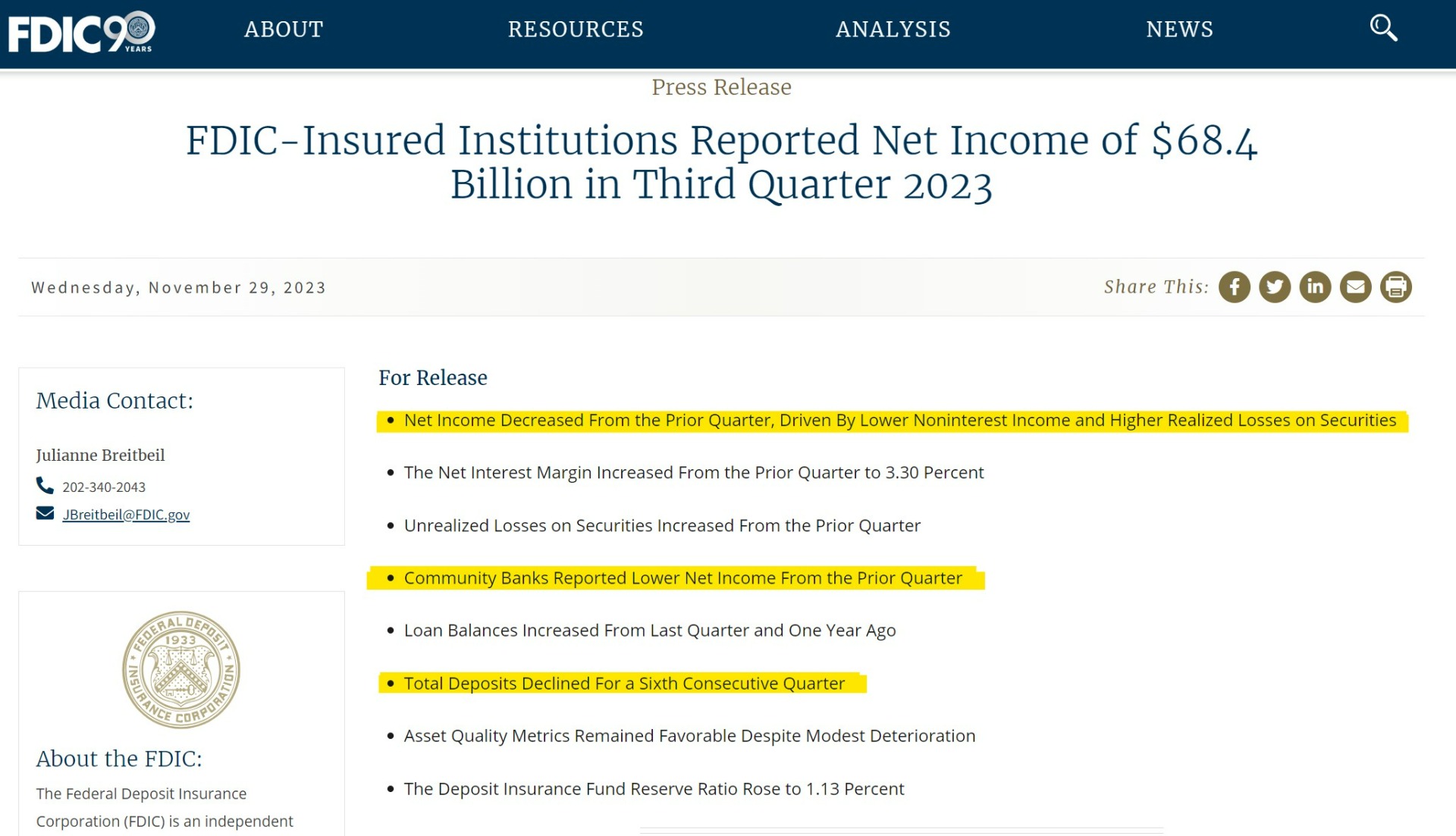

The latest FDIC data also reveals other important key facts about the state of the US banking system. Let's look at the first thing the FDIC says. Net income decreased compared to the previous quarter due to lower interest income and higher realized losses on securities.

It is very interesting and worthy of attention and thought that after the third quarter, the mainstream media tried to point to the good performance of the banks, where without the need to understand what was actually happening, they praised how the profits of the banking sector increased due to higher interest rates ... And did not inform nor about the said failure of Heartland Tri-State Bank and Citizens Bank…

Commercial banks reported a generally lower net profit compared to the previous quarter. There's quite a bit of concern around small to mid-sized banks and their ability to cover what's happening with interest rates, with their real estate portfolio and the economy in general. Based on this, I would venture to say that we will soon hear about other commercial banks not being able to manage six consecutive quarters of declines in deposits and profits, as indicated by the FDIC report.

The FDIC report said the decline in net income from the previous quarter was due to lower non-interest income and higher realized losses on securities. At 4,614 commercial banks and savings banks, third-quarter net income fell $2.4 billion from the previous quarter, to $68.4 billion. The likelihood of further declines in profits and problems for commercial banks will continue to be high as small to mid-sized banks need to obtain additional liquidity and are thus forced to sell their undervalued securities at a loss. And needless to say, if the Fed decides to raise rates again, these unrealized losses will continue to grow. The longer the Fed keeps rates high, the longer the banks will have to use the Fed bailout program and borrow against their impaired assets.

A week ago, the rating agency Moody's also issued a negative outlook for the entire global banking sector for 2024 - "2024 Outlook negative as tied Financial conditions and economic slowdown sting".

Moody'sexpressed its negative outlook based on a deteriorating environment, an increase in non-performing loans and the likelihood of widespread conflict in the Middle East. The agency further believes that if this conflict widens, there are real risks to the oil market as well as overall market sentiment. Moody's also states that the tighter monetary policy of central banks also led to lower GDP growth.

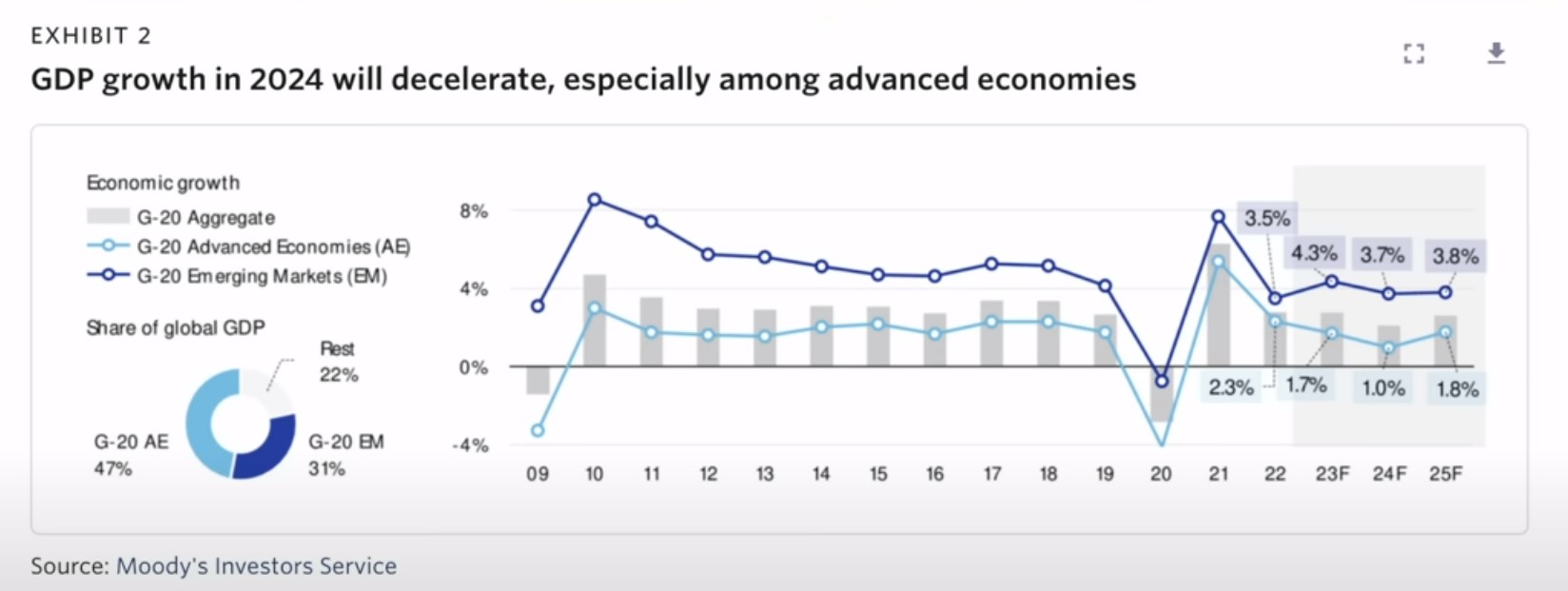

It is increasingly clear that global growth will be either negative or extremely slow next year, while we will see a further increase in commercial and personal loan defaults, which will occur as a result of low liquidity. In other words, there is less cash available and, of course, a reduced ability to repay. In general, the rating agency believes that GDP growth among advanced economies will decelerate rapidly in 2024.

The rating agency further expects finances to remain very tight next year, as sentiment due to tight credit conditions does not give much hope for economic growth at all.

Even if banks started to cut rates, it would probably not have any major positive effect in 2024.

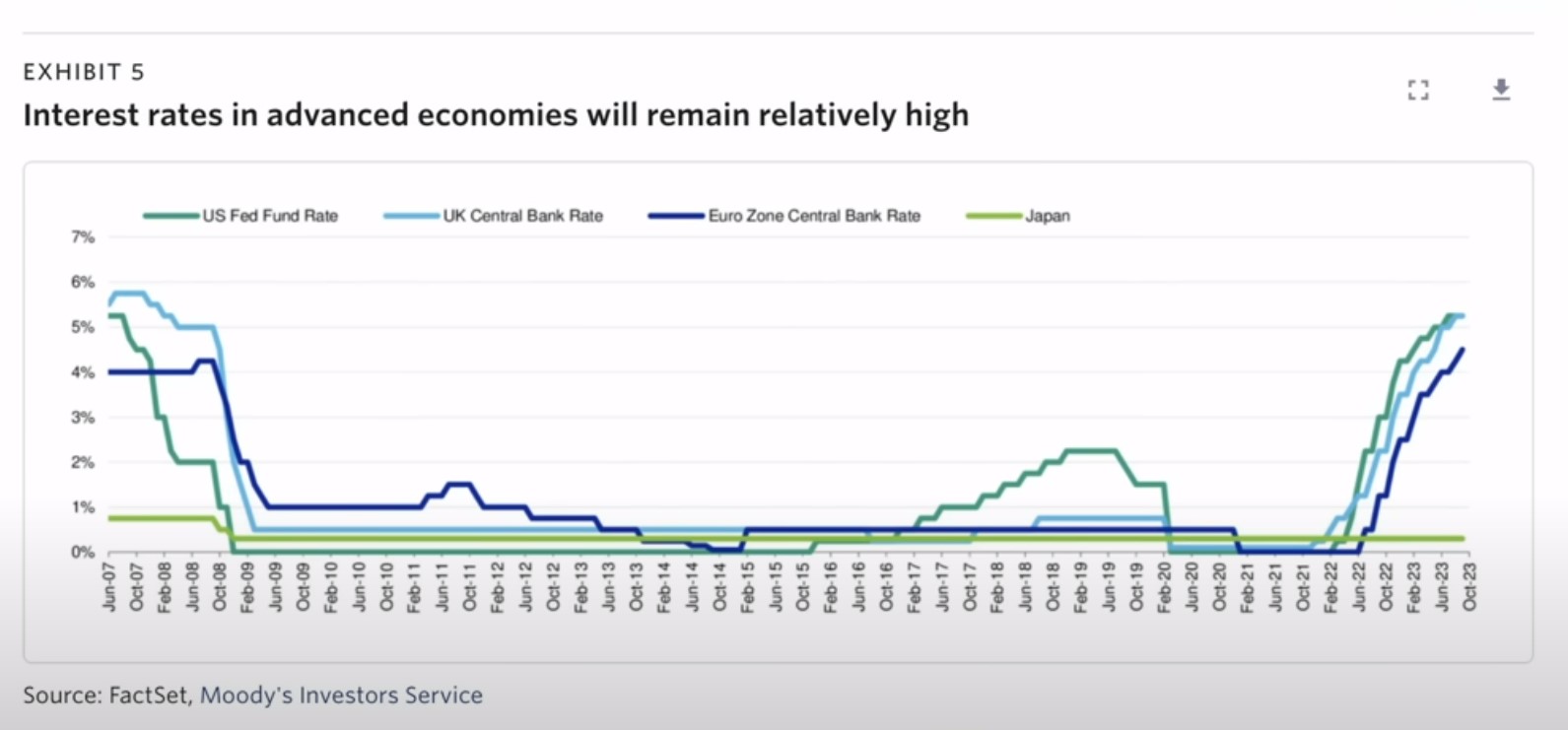

Conversely, Moody's says interest rates will remain high in advanced economies. He further predicts that the areas that will be affected the most will be Africa and the Middle East, where he already sees a rise in bad loans. These banking shocks will not only affect developing countries, but developed countries will also feel the consequences. Moody's says falling consumer confidence and a rise in unemployment could lead to a surge in bad loans in the UK and Canada as well, pointing out that the biggest problem areas in the US are commercial real estate and private credit funds.

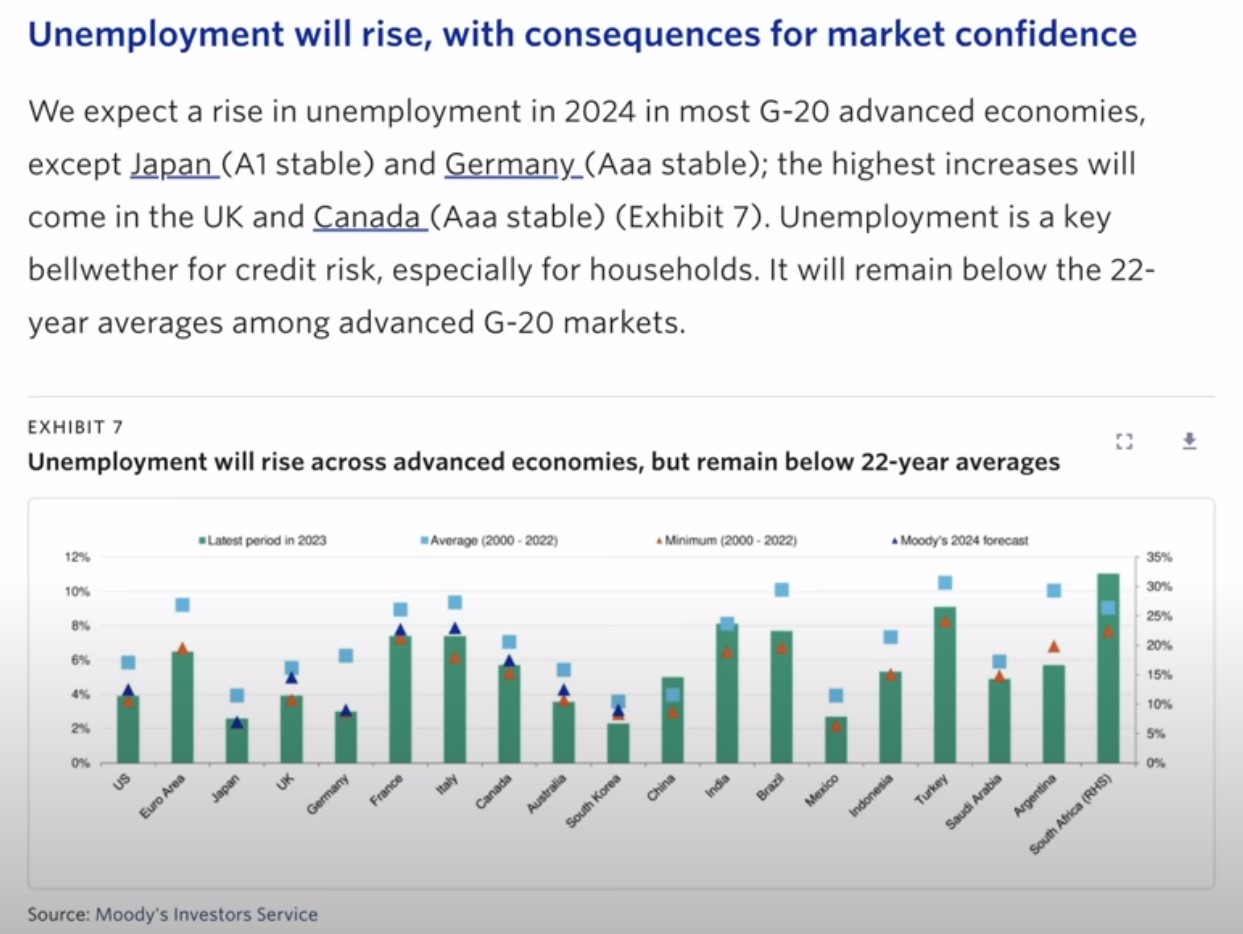

The agency fears that multiple rate hikes will lead to higher unemployment even in the G20 countries, and as we know, higher unemployment will in turn lead to an increase in loan defaults. Unemployment growth in 2024 can be expected in most advanced G20 economies with the exception of Japan and Germany.

Moody's also states that unemployment is a key litmus test for credit risk, especially for households, as we can see here in this chart.

Moody's expects unemployment to be around 10% in the US next year, with France and Italy seeing increases above 20%, and significant increases for Turkey, Brazil and India.

In its Outlook 2024, Moody's highlights that consecutive multiple rate hikes by central banks and rising unemployment in advanced economies will weaken asset quality, which is the main reason why we need to be aware of the risks associated with excessive exposure of US and European banks to real estate. Moody's has admitted that banks have had a rather mixed performance this year, where income was primarily driven by higher interest rates, but this is not sustainable in the long term, and banks will thus run into liquidity problems.

Liquidity concerns have focused mainly on small and medium-sized banks, while the largest US banks are likely to continue to build and strengthen their capital, Moody's said.

Moody's is very concerned about the growth of loan defaults and the possibility that these loan defaults will spiral out of control. If unemployment numbers begin to rise, it is highly likely that the full impact of multiple rate hikes in the United States and Europe is yet to be felt. And if other circumstances arise, such as a war in the Middle East or some other unforeseen event, the banks that already have liquidity problems will be the first/next to fail.

Michal